VA Debt-to-Income Ratios: How Much Can You Borrow?

VA loans are more flexible on debt-to-income ratio than conventional or FHA loans, but DTI still plays a critical role in determining how much you can borrow. Understanding how the VA calculates DTI and what residual income means will help you maximize your borrowing power and position yourself for approval.

VA loans are more flexible on debt-to-income ratio than conventional or FHA loans, but DTI still plays a critical role in determining how much you can borrow. Understanding how the VA calculates DTI and what residual income means will help you maximize your borrowing power and position yourself for approval.

VA DTI Guidelines

The 41% Rule

Preferred DTI: 41% or lower

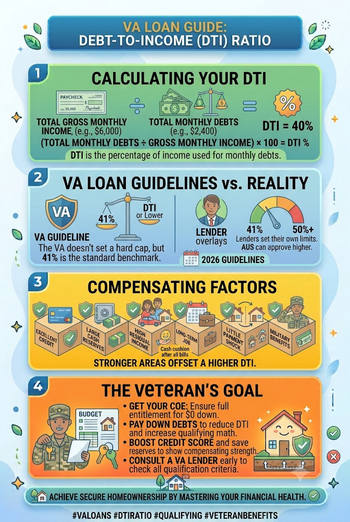

The VA's preferred guideline is that your total monthly debt payments (including the new mortgage) should not exceed 41% of your gross monthly income.

Example: If you earn $6,000/month gross, your total monthly debt should not exceed $2,460.

Above 41% (The Flexibility Zone)

Acceptable DTI: 41-50% with compensating factors

The VA allows lenders to approve DTI ratios above 41% if you have compensating factors. Many VA lenders routinely approve borrowers with DTI up to 50% if:

- Excellent credit score (740+)

- Large cash reserves (6+ months of payments)

- Stable, long-term employment

- Strong residual income (discussed below)

- Recent pay increases or strong income growth

Example: You have a 48% DTI but excellent credit (760+), $50,000 in savings, and have worked at the same employer for 8 years. Lenders will likely approve you despite the high DTI.

Above 50% (Very Difficult)

DTI 50-60%: Possible but difficult; approval requires very strong compensating factors

DTI above 60%: Most lenders will decline your application

What Makes VA DTI Different: Residual Income

This is where VA loans really stand out. The VA doesn't just look at DTI percentage - they also evaluate residual income.

What is Residual Income?

Residual income is the amount of money left over each month after you pay all your debts and living expenses. It's a safety cushion that shows you can handle unexpected financial problems.

Residual Income Formula

Residual income = Gross monthly income - Total monthly debt - Living expenses

Example Calculation

Gross monthly income: $6,000

Total monthly debt (new mortgage + car + credit cards): $2,500

Living expenses (utilities, food, insurance, etc.): $2,000

Residual income = $6,000 - $2,500 - $2,000 = $1,500/month

You have $1,500/month left over after all obligations. This is your residual income.

Why Residual Income Matters

Residual income shows you're not living paycheck to paycheck. It demonstrates financial stability and your ability to handle emergencies.

High residual income: Even if your DTI is 48%, lenders are comfortable because you have substantial cushion

Low residual income: Even if your DTI is 40%, lenders may be concerned if you have little left over

VA Residual Income Guidelines

The VA publishes residual income requirements that vary by family size and region. Here are 2025 guidelines:

| Family Size | Northeast | Midwest | South | West |

|---|---|---|---|---|

| 1 | $450 | $425 | $400 | $475 |

| 2 | $750 | $700 | $675 | $800 |

| 3 | $925 | $875 | $850 | $975 |

| 4 | $1,100 | $1,050 | $1,000 | $1,150 |

| 5 | $1,275 | $1,200 | $1,150 | $1,325 |

These are minimums. Your residual income should meet or exceed these amounts for your family size and region.

How Lenders Use Residual Income

If your DTI is above 41%, lenders will check your residual income. If it exceeds the VA guideline for your family size and region, you get approved despite the high DTI.

Example: You're a family of 3 in the Midwest. Your DTI is 48% (above the preferred 41%), but your residual income is $1,200/month. The VA guideline for your situation is $875. Since $1,200 exceeds the guideline, lenders will approve you despite the high DTI.

VA DTI Limits in Real Numbers

Example 1: Single, Good Financial Position

Income: $5,000/month

41% DTI limit: $2,050

Current debts: $300 (car loan)

Available for mortgage: $1,750

At 6.5% interest: ~$285,000 borrowing power

Example 2: Family of 4, Higher Income

Combined income: $8,000/month

41% DTI limit: $3,280

Current debts: $600 (car + student loans)

Available for mortgage: $2,680

At 6.5% interest: ~$440,000 borrowing power

Example 3: Above 41% DTI with Strong Residual Income

Income: $6,500/month

DTI: 48% (higher than preferred 41%)

Total debt allowed: $3,120

Current debts: $600

Available for mortgage: $2,520

At 6.5% interest: ~$410,000 borrowing power

BUT: Check residual income. If family of 4 in Midwest with residual income of $1,100 (exceeds $1,050 guideline), approval is likely despite 48% DTI.

How to Calculate Your Maximum VA Loan Amount

Step 1: Calculate Your Maximum Debt Capacity

Multiply your gross monthly income by 41% (or your lender's DTI limit).

Gross monthly income: $6,000

Maximum debt at 41%: $6,000 × 0.41 = $2,460

Step 2: Subtract Existing Monthly Debts

Current debts: $300 (car) + $150 (student loans) + $100 (credit cards) = $550

Available for mortgage: $2,460 - $550 = $1,910

Step 3: Convert Monthly Payment to Loan Amount

Use a mortgage calculator or this rough formula:

Loan amount ≈ Monthly payment × 164 (at 6.5% interest)

$1,910 × 164 ≈ $313,000 borrowing power

Step 4: Verify Residual Income (If DTI > 41%)

If your DTI is above 41%, calculate residual income:

Residual = Income - (New mortgage payment + existing debts) - Living expenses

Residual = $6,000 - $1,910 - $2,000 = $1,090

Compare to VA guidelines for your family size and region. If residual income is adequate, you're approved despite a high DTI.

VA DTI Flexibility: Real-World Scenarios

Scenario 1: Above 41% DTI But Strong Residual Income

You: Family of 4, earning $7,500/month gross

DTI: 45% (above preferred 41%)

Maximum debt: $3,375

Current debts: $600

Mortgage payment: $2,775

Residual income: $7,500 - $3,375 - $2,000 = $2,125

VA guideline for family of 4 in South: $1,000

Result: Your residual income ($2,125) exceeds the guideline ($1,000), so you're approved despite 45% DTI.

Scenario 2: 41% DTI But Low Residual Income

You: Single, earning $5,000/month gross

DTI: 41% (at preferred limit)

Maximum debt: $2,050

Current debts: $1,000 (multiple debts)

Mortgage payment: $1,050

Residual income: $5,000 - $2,050 - $2,500 = $450

VA guideline for family of 1 in Midwest: $425

Result: You're barely above the residual income guideline ($450 vs. $425), so you're approved at 41% DTI.

Scenario 3: Too High DTI, Low Residual Income

You: Family of 3, earning $6,000/month gross

DTI: 50% (significantly above 41%)

Maximum debt: $3,000

Current debts: $1,000

Mortgage payment: $2,000

Residual income: $6,000 - $3,000 - $2,500 = $500

VA guideline for family of 3 in South: $850

Result: Residual income ($500) falls short of guideline ($850). Approval is difficult without strong compensating factors (excellent credit, large savings, etc.).

Compensating Factors for High DTI

If your DTI is above 41% and your residual income is marginal, lenders look for compensating factors:

Strong Compensating Factors

- Excellent credit score (760+): Shows you manage debt responsibly

- Very large cash reserves (9+ months of payments): Significant financial cushion

- Long-term stable employment (8+ years): Job security

- Recent significant income increase: Shows future financial capacity

- Strong down payment (10%+): Reduces lender risk

- Equity in other properties: Shows successful real estate history

Moderate Compensating Factors

- Good credit score (720-759)

- Adequate cash reserves (6-9 months)

- Stable employment (4-8 years)

- Small down payment (5-10%)

- Recent pay increase

Strategies to Improve Your VA DTI

Strategy 1: Pay Down Credit Cards (Fastest Impact)

Paying down credit card balances reduces your minimum payments and improves DTI immediately.

Impact: Each $5,000 paid off saves ~$100/month in minimum payments, improving DTI by 1.7% (assuming $6,000 income)

Timeline: 1-3 months with aggressive paydown

Strategy 2: Increase Your Income

A higher income increases the denominator of your DTI calculation, allowing more debt.

Example: Increasing income by $1,000/month improves your DTI by 3.3% (assuming 41% calculation)

Timeline: Immediate with new job; gradual with raises

Strategy 3: Reduce the Loan Amount You're Requesting

A smaller mortgage payment improves your DTI.

Impact: Reducing loan amount by $50,000 (~$330/month payment) improves DTI by 5.5%

Timeline: Immediate, but you have less buying power

Strategy 4: Pay Off Debt Entirely

Eliminating debts completely removes them from your DTI calculation.

Impact: Paying off a $400/month car loan improves DTI by 6.7%

Timeline: Depends on remaining balance

Strategy 5: Wait and Build Residual Income

If your DTI is high but residual income is low, waiting while saving and paying down debt improves both metrics.

Timeline: 6-12 months, but most comprehensive improvement

VA DTI vs. Other Loan Types

| Loan Type | Preferred DTI | Acceptable DTI | Special Consideration |

|---|---|---|---|

| VA Loan | 41% | 41-50% | Residual income can overcome high DTI |

| FHA Loan | 31% front-end | 43-50% back-end | Front-end (housing only) is strict |

| Conventional Loan | 28% front-end | 36-43% back-end | Most restrictive of all |

Key Takeaways

- VA preferred DTI is 41%. This is the target, but not a hard limit.

- VA allows DTI up to 50% with compensating factors. More flexible than conventional or FHA.

- Residual income is critical for high DTI. It demonstrates financial stability beyond just the percentage.

- VA publishes residual income guidelines by family size and region. Your residual income should meet or exceed these.

- High residual income can overcome slightly high DTI. This is unique to VA loans.

- Paying down credit cards improves DTI fastest. Target cards with highest minimum payments.

- Income increases improve DTI immediately. Every $1,000 more monthly income helps significantly.

- DTI directly determines your borrowing power. Every percentage point is worth $30,000-$50,000 in loan amount.

- Compensating factors matter for approval. Excellent credit, large savings, and stable employment help overcome high DTI.

- Compare residual income to guidelines. Meeting guidelines even at high DTI improves approval odds.

Bottom Line

VA loans are uniquely flexible on debt-to-income ratio because they consider both DTI percentage and residual income. This means you might get approved with a 48% DTI if your residual income is strong- something conventional lenders would deny immediately. Understand your DTI, calculate your residual income, and know the VA guidelines for your family size and region. If you're above 41% DTI, focus on improving residual income through debt paydown and savings. The VA's flexibility can work in your favor if you understand how they evaluate your financial picture.

Connect With Us

Please share – it really helps