Conventional ARM Loans: How Adjustable Rates Work

If

you’re considering buying a home or refinancing, understanding

your loan options is crucial. One choice that often comes up is

a conventional loan with an adjustable-rate mortgage (ARM).

If

you’re considering buying a home or refinancing, understanding

your loan options is crucial. One choice that often comes up is

a conventional loan with an adjustable-rate mortgage (ARM).

You might wonder how this loan works and if it’s the right fit for your financial goals. Imagine starting with lower monthly payments that can change over time - this flexibility can save you money early on, but also carries some risks.

You’ll discover how a conventional ARM works, its benefits, and what to watch out for. Keep reading to make a confident decision that suits your budget and plans.

Basics Of Conventional Loans

Conventional loans are a common type of home mortgage. The government does not back them. Borrowers choose them for their flexibility and wide availability. These loans usually require good credit scores and stable incomes.

Conventional loans can have fixed or adjustable interest rates. The adjustable-rate mortgage, or ARM, starts with a lower interest rate. This rate changes over time in response to market conditions. Understanding the basics of conventional loans helps in making smart decisions.

What Is A Conventional Loan?

A conventional loan is a mortgage not insured by the government. Banks and lenders offer these loans directly. They often require higher credit scores than government loans. Borrowers must prove their ability to repay the loan.

Key Features Of Conventional Loans

These loans typically need a down payment of at least 3%. Borrowers may choose between fixed or adjustable rates. Loan amounts usually follow limits set by government agencies. Conventional loans offer flexible terms and options.

Who Qualifies For A Conventional Loan?

Good credit scores and a steady income help in qualifying. Lenders look for low debt-to-income ratios. Borrowers must provide proof of income and assets. Conventional loans suit buyers with strong financial profiles.

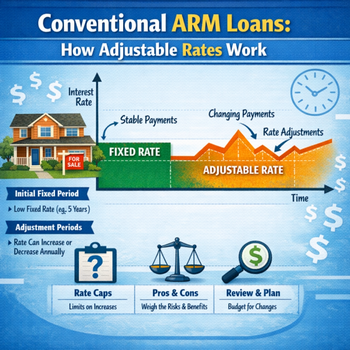

How Adjustable Rate Mortgages Work

An Adjustable Rate Mortgage (ARM) is a type of conventional loan with an interest rate that changes over time. This loan starts with a fixed rate for a set period. After this period, the interest rate adjusts at regular intervals based on a specific index.

The initial fixed-rate period can last from a few months to several years. After this, the rate can go up or down depending on market conditions. This means your monthly payments may increase or decrease.

Initial Fixed-rate Period

This period offers a low, stable interest rate. It usually lasts 3, 5, 7, or 10 years. During this time, your monthly payment stays the same. It helps with budgeting and planning.

Adjustment Period

After the fixed period, the rate adjusts. Adjustments occur every 6 or 12 months. The new rate depends on an index plus a margin set by the lender. This makes your payments flexible.

Interest Rate Caps

Caps limit how much your rate can change. They protect you from big increases. Caps apply to each adjustment and over the loan’s life. This keeps your payments predictable.

Index And Margin

The index reflects current market interest rates. Common indexes include the LIBOR or U.S. Treasury rates. The margin is a fixed percentage added to the index. The sum determines your new interest rate.

Payment Changes

Your monthly payment changes with interest rate adjustments. If rates go down, payments drop. If rates rise, payments increase. Knowing this helps you manage your budget.

Initial Rate Period Explained

The initial rate period is the first phase of an Adjustable Rate Mortgage (ARM). During this time, the interest rate stays fixed. It does not change, giving borrowers stable monthly payments. This period can last from a few months up to several years, depending on the loan terms.

This fixed period offers a lower interest rate compared to fixed-rate loans. Borrowers benefit from reduced payments early in the mortgage. After this period ends, the rate adjusts periodically based on market conditions. Understanding the initial rate period helps buyers plan their finances better.

What Is The Length Of The Initial Rate Period?

The length varies by loan type. Common periods last 3, 5, 7, or 10 years. A 5/1 ARM, for example, has a fixed rate for five years. Afterward, the rate is adjusted once a year. Choosing the right length depends on your financial plans and how long you expect to keep the home.

How Is The Initial Rate Set?

The initial rate usually starts lower than fixed mortgage rates. Lenders offer this as an incentive to attract borrowers. It is based on current market rates and borrower creditworthiness. This rate stays the same throughout the initial period, offering payment stability.

Benefits Of The Initial Rate Period

Borrowers enjoy lower monthly payments initially. This can make homeownership more affordable at the start. It helps buyers qualify for larger loans or better homes. The stability during this time reduces financial stress. It also gives time to improve credit or save money before rates adjust.

What Happens After The Initial Rate Period?

Once the initial period ends, the rate changes. It adjusts based on an index plus a margin set by the lender. Payments can go up or down depending on market rates. Caps limit how much the rate can increase at each adjustment. Understanding this helps prepare for future payment changes.

Rate Adjustment And Caps

An adjustable-rate mortgage (ARM) features interest rates that change over time. This change happens at specific intervals called rate adjustments. Understanding how rate adjustments and caps work helps homeowners plan their finances better.

Rate adjustments mean your loan’s interest rate can rise or fall. The change depends on the market index the loan follows. Lenders add a fixed margin to this index to determine your new rate. This new rate affects your monthly mortgage payments.

What Is A Rate Adjustment?

Rate adjustment is when the lender changes your mortgage interest rate. These changes usually happen yearly or after an initial fixed period. The timing depends on your loan’s terms. Each adjustment updates your rate based on the current market index.

This adjustment affects your monthly payments. Payments can increase or decrease. This makes ARMs different from fixed-rate loans, which keep the same rate throughout.

How Rate Caps Protect Borrowers

Rate caps limit how much your interest rate can change. Caps prevent sudden, large increases in your mortgage payments. They protect borrowers from big financial shocks.

There are different types of caps. Periodic caps limit rate changes at each adjustment. Lifetime caps set a maximum rate over the loan’s life. Both help keep payments manageable.

Understanding Initial, Periodic, And Lifetime Caps

The initial cap limits the first rate increase after the fixed period. Periodic caps control increases for each adjustment period. Lifetime caps set the highest rate your loan can reach.

Knowing these caps helps you predict potential changes in payments. It also helps you decide if an ARM fits your budget and risk tolerance.

Pros Of Adjustable Rate Mortgages

Adjustable Rate Mortgages (ARMs) have unique benefits that attract many homebuyers. These loans start with a lower interest rate than fixed-rate mortgages. This can lead to smaller monthly payments during the initial period. ARMs provide flexibility for those who plan to move or refinance before rates adjust.

Understanding the advantages helps to decide if an ARM suits your financial goals. Here are the key pros of Adjustable Rate Mortgages.

Lower Initial Interest Rates

ARMs often offer lower starting rates than fixed loans. This means lower payments at the beginning of the loan. It helps buyers afford a home or save money early on.

Potential For Decreased Rates

The interest rate can go down after the fixed period. This can reduce monthly payments over time. Borrowers may benefit if market rates drop.

Flexibility For Short-term Plans

ARMs suit buyers who sell or refinance within a few years. The initial low rate saves money during that time. It avoids paying higher fixed rates on longer loans.

Smaller Monthly Payments Initially

Lower rates lead to smaller monthly payments at first. This makes budgeting easier for new homeowners. They can use savings for other expenses or investments.

Cons Of Adjustable Rate Mortgages

An adjustable-rate mortgage (ARM) offers a lower initial interest rate than a fixed-rate mortgage. This can seem attractive at first. Yet, ARMs come with risks that may cause financial strain. Understanding the cons is important before choosing this loan type.

The Risk Of Rising Interest Rates

Interest rates can increase after the initial fixed period. Higher rates mean higher monthly payments. This can make budgeting difficult for homeowners. Sudden payment hikes might lead to missed payments or loan default.

Payment Uncertainty

Monthly payments can often change with an ARM. This makes long-term financial planning hard. Homeowners may find it stressful not knowing what payments will be. Fixed payments offer more stability and peace of mind.

Complex Terms And Conditions

ARMs have complicated rules about rate changes. Caps, margins, and indexes affect the interest rate. Many borrowers find these terms confusing. Misunderstanding the loan details can lead to costly mistakes.

Potential For Negative Amortization

Some ARMs allow payments that do not cover interest. The unpaid interest adds to the loan balance. This means owing more than the original loan amount. Negative amortization can increase debt and risk of foreclosure.

Limited Benefit For Long-term Homeowners

ARMs are best for short-term homeownership or refinancing. Those staying long-term may pay more over time. Fixed-rate mortgages often prove cheaper for long stays. Adjustable rates can end up costing more in total interest.

Choosing Between an ARM and a Fixed Rate

Choosing between an Adjustable Rate Mortgage (ARM) and a Fixed Rate loan is a key decision for homebuyers. Each option has unique features that affect monthly payments and long-term costs. Understanding these differences helps in selecting the best mortgage for your financial situation and plans.

What Is An Adjustable Rate Mortgage?

An ARM starts with a lower interest rate than a fixed loan. This rate stays the same for a set period, usually 3, 5, or 7 years. After that, the rate changes based on market conditions. Your monthly payments can go up or down over time.

Benefits Of Fixed Rate Mortgages

Fixed-rate loans keep the same interest rate for the entire term. This means your monthly payments remain stable. It offers peace of mind and easier budgeting. Fixed loans are ideal for those who plan to stay in their home for a long time.

When To Choose An Arm

Choose an ARM if you want lower initial payments. This works well if you plan to sell or refinance before rates adjust. ARMs can save money early on, but they carry the risk of higher costs later.

Factors To Consider Before Deciding

Think about how long you will live in the home. Consider your tolerance for payment changes. Look at current interest rates and market trends. Also, review your financial stability and future income prospects.

Frequently Asked Questions

What Is A Conventional Adjustable-rate Mortgage?

A conventional adjustable-rate mortgage (ARM) starts with a fixed lower interest rate. The rate adjusts periodically based on market indexes, affecting monthly payments. It combines initial affordability with the possibility of future rate changes, unlike fixed-rate mortgages, which keep the same rate throughout the loan term.

Will Mortgage Rates Go Down To 5% In 2027?

Mortgage rates depend on economic factors and Federal Reserve policies. Predicting a 5% rate by 2027 remains uncertain. Monitor market trends and expert forecasts for updates.

What Is The 2% Rule for Refinancing?

The 2% rule for refinancing means your new loan's interest rate must be at least 2% lower than your current rate to save money. This helps determine if refinancing is financially beneficial by reducing monthly payments and overall interest costs.

Can a 70-year-old woman get a 30 Year Mortgage?

Yes, a 70-year-old woman can get a 30-year mortgage. Lenders consider income, credit, and repayment ability.

What Is A Conventional Adjustable-rate Mortgage (ARM)?

A conventional ARM is a home loan with a fixed initial rate. After that, the interest rate changes periodically in response to market conditions. It usually starts lower than fixed-rate loans.

Conclusion

Choosing a conventional loan with an adjustable-rate mortgage can offer initial savings. The interest rate starts low but may increase over time. This type of loan suits buyers who plan to move or refinance before rates rise. Understanding how rates adjust helps avoid surprises.

Always compare options to find what fits your budget best. Keep track of rate changes during the loan term. A clear plan can make ARM loans work well. Consider your financial goals carefully before deciding.

Connect With Us

Please share – it really helps