How Much Are VA Funding Fees?

Are

you considering using a VA loan to purchase a home, but are unsure

about the costs involved? One key factor to consider is the VA

funding fee. In this article, we will explore how much VA funding

fees typically cost and how they can impact your overall loan

amount. Let's dive in and learn more about how much VA funding fees

are and what you need to know before applying for a VA loan.

Are

you considering using a VA loan to purchase a home, but are unsure

about the costs involved? One key factor to consider is the VA

funding fee. In this article, we will explore how much VA funding

fees typically cost and how they can impact your overall loan

amount. Let's dive in and learn more about how much VA funding fees

are and what you need to know before applying for a VA loan.

Key Takeaways

- VA funding fees are mandatory charges the Department of Veterans Affairs (VA) imposes on veterans or borrowers using VA loans.

- VA funding fees are intended to offset the cost of administering the VA loan program, support programs and services for veterans, and sustain and support the VA loan program for eligible veterans.

- The calculation of VA funding fees considers factors such as loan amount, interest rate, and loan type.

- Higher loan amounts result in higher funding fees.

- Exemptions and waivers for VA funding fees are available for veterans with disabilities, Purple Heart recipients, surviving spouses of service members who died in the line of duty, and active-duty military members. Veterans facing financial hardship can also seek arrangements from the VA.

Definition of VA Funding Fees

The Department of Veterans Affairs (VA) levies mandatory fees as a requirement for financing through the VA loan program. Veterans or borrowers utilizing VA loans to buy or refinance their homes are responsible for paying these fees.

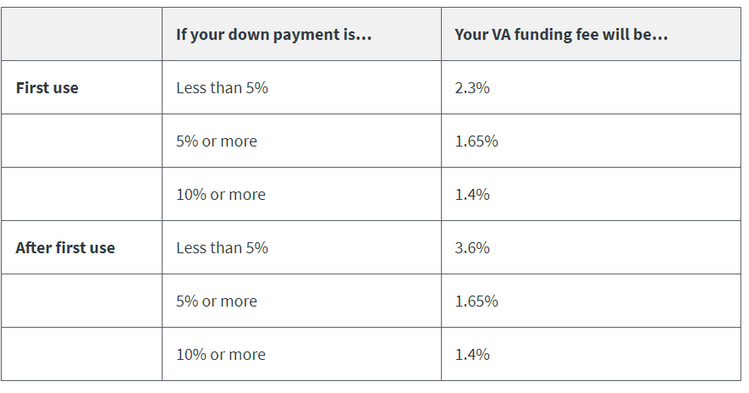

The funding fee varies depending on the type of loan, the down payment amount, and whether it's the borrower's first or subsequent use of the VA mortgage program. Veterans, active-duty service members, and surviving spouses of veterans are eligible for VA funding fees.

The funding fee is calculated as a percentage of the loan amount, with exemptions available for specific individuals, such as those with service-connected disabilities or receiving disability compensation.

Purpose of VA Funding Fees

VA funding fees are a vital financial contribution for veterans and borrowers utilizing the VA financing program. The primary purposes of these fees include:

- Supporting eligible veterans: The fees collected from VA loans contribute to funding various programs and services offered to veterans, encompassing healthcare, education, and housing assistance.

- Evaluating borrowers' circumstances: VA funding fees play a role in assessing borrowers' creditworthiness and financial stability, ensuring that the loan program remains accessible to those who genuinely need it.

- Loan eligibility requirements: VA funding fees are integral to the loan eligibility requirements, signifying the borrower's commitment to the loan and ability to fulfill financial obligations.

- Eliminating mortgage insurance: VA funding fees negate the need for private mortgage insurance, typically required for conventional loans, providing borrowers with a more affordable financing option.

While specific individuals may be exempt from VA funding fees, the fees sustain and support the VA loan program, which benefits all eligible veterans.

Types of VA Funding Fees

VA funding fees encompass various categories associated with VA loans, with exemptions available for veterans with disabilities. These fees differ based on the type of loan and the borrower's circumstances.

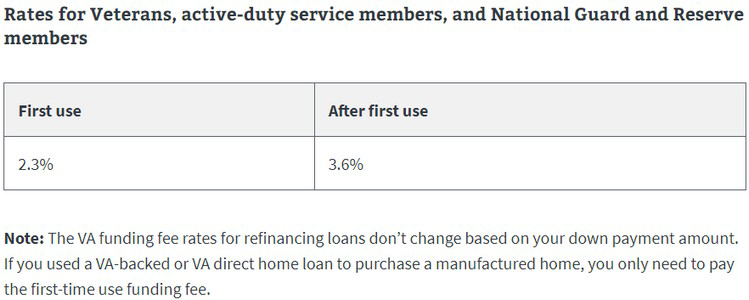

For instance, home purchase loans may incur funding fees ranging from 1.4% to 3.6% of the mortgage amount, contingent upon the borrower's down payment and previous use of VA loan benefits. Cash-out refinance loans typically entail a funding fee of 2.3% of the mortgage amount.

The funding fee is typically paid at loan closing but can also be financed into the loan amount, although borrowers should consider these fees when evaluating their financing options.

How Are VA Funding Fees Calculated?

The calculation of VA funding fees considers several factors, including the loan type, financing amount, and borrower's down payment. The key factors influencing VA funding fee calculations include:

- Loan amount: VA funding fees are calculated as a percentage of the loan amount, with higher loan amounts resulting in higher funding fees.

- Interest rate: The funding fees vary based on whether the borrower is a first-time or repeat homebuyer, the loan term, and the down payment amount.

- Loan type: The type of VA loan, whether a purchase or refinance loan, can impact the funding fee calculation.

- Exemptions: Certain individuals, such as veterans with service-connected disabilities, may be eligible for waivers from the funding fee.

Understanding how VA funding fees are calculated is essential for prospective homebuyers seeking VA financing. It enables them to assess their financing options and associated costs accurately.

Exemptions and Waivers for VA Funding Fees

Individuals may qualify for exemptions and waivers from VA funding fees, with eligibility criteria based on various factors, including disability ratings and military service history.

Veterans with a service-connected disability of at least 10% are typically exempt from paying the VA funding fee, along with Purple Heart recipients. Additionally, surviving spouses of service members who died in the line of duty or due to a service-connected disability may also qualify for an exemption.

Active-duty military members and veterans facing financial hardship may be eligible for waivers or arrangements from the VA to alleviate the burden of funding fees.

Understanding the impact of VA funding fees on loan financing is crucial for borrowers, as is exploring available exemptions and waivers to minimize financial obligations.

Importance of VA Funding Fees for the VA Loan Program

VA funding fees play a pivotal role in ensuring the viability and sustainability of the VA Loan Program, benefiting eligible veterans and service members in several ways:

- Supporting the VA Home Loan Program: Funding fees finance the program, enabling it to offer affordable home loans to eligible VA borrowers.

- Ensuring Fairness: By charging fees, the VA Loan Program ensures that all borrowers contribute to its costs, promoting fairness and equity in loan accessibility.

- Lower Mortgage Interest Rates: The fees help offset program costs, allowing the VA to provide lower mortgage interest rates to borrowers.

- Funding Down Payment Assistance Programs: A portion of the fees supports down payment assistance programs, making homeownership more accessible for first-time and repeat homebuyers.

Understanding the importance of VA funding fees underscores the value and benefits provided by the VA Loan Program to eligible veterans and service members.

Comparing VA Funding Fees to Other Mortgage Fees

Comparing VA funding fees to other mortgage fees provides insights into their relative cost and impact on borrowers. While mortgage fees encompass various expenses associated with loan acquisition, VA funding fees specifically support the administration of the VA home loan program.

Although VA funding fees are typically lower than closing costs for conventional loans, they can be financed into the loan amount, reducing immediate out-of-pocket expenses for eligible borrowers. Additionally, funding fees are significantly reduced for those qualifying for an Interest Rate Reduction Refinance Loan (IRRL), benefiting borrowers.

Tips for Managing VA Funding Fees

Effectively managing VA funding fees requires careful planning and consideration. Here are four tips to help borrowers navigate these fees:

- Understand VA loan program eligibility: Ensure eligibility requirements are met before applying for a VA loan to avoid unnecessary fees and complications.

- Research and compare lenders: Different lenders may offer varying funding fee structures, so research and compare options to find the most favorable terms.

- Estimate closing costs: Request closing cost estimates from potential lenders to plan your budget accurately, including funding fees.

- Consider the impact on mortgage payment: Recognize that the funding fee is typically added to the loan amount, increasing the mortgage payment, mainly if no down payment is made.

Funding Fee Chart

VA Cash Out Chart

Conclusion: How Much Are VA Funding Fees?

In conclusion, understanding the implications of VA funding fees is crucial for anyone looking to utilize a VA loan for home purchase. The costs associated with these fees can vary depending on several factors, but being aware of them upfront can help you better plan your budget and financial strategy. By knowing how much VA funding fees typically cost and how they factor into your loan amount, you can make informed decisions about your home buying process.

Before applying for a VA loan, it's important to thoroughly research and consider all potential expenses involved, including the funding fee. Take the time to consult with a knowledgeable lender or financial advisor to ensure you are fully prepared for the costs associated with using a VA loan.

Connect With Us

Please share – it really helps