Conventional Loan Credit Score Requirements for Approval

For

most American homebuyers, the "conventional loan"—a mortgage not

insured or guaranteed by the federal government (like FHA, VA,

or USDA)—is the gold standard. It often offers the best interest

rates, lower overall costs, and more flexible terms.

For

most American homebuyers, the "conventional loan"—a mortgage not

insured or guaranteed by the federal government (like FHA, VA,

or USDA)—is the gold standard. It often offers the best interest

rates, lower overall costs, and more flexible terms.

But before you can unlock those benefits, you have to pass through the gateway: the credit score.

While the minimum number to qualify might be lower than you think, the score you actually need to make a conventional loan financially worthwhile is often significantly higher. Here is everything you need to know about the credit score requirements for conventional loans, how lenders view your score, and what you can do to improve it.

The Baseline: What is the Minimum Score?

The entities that set the rules for most conventional loans are Fannie Mae and Freddie Mac. These government-sponsored enterprises (GSEs) buy loans from lenders, and they set the underwriting standards.

- The Official Minimum: For a conventional loan backed by Fannie Mae or Freddie Mac, the minimum credit score is typically 620.

However, reaching 620 is merely the starting line. Just because you can get a loan with a 620 doesn’t mean you should settle for that number. Lenders may overlay their own requirements on top of Fannie and Freddie’s guidelines. Many lenders will set their own minimum at 640 or 660 to reduce their risk.

The Tiers: How Scores Affect Your Wallet

In the world of conventional lending, your credit score is the primary driver of your interest rate. Lenders use a system called Loan-Level Price Adjustments (LLPAs). Essentially, the lower your credit score, the higher your interest rate—and the more you pay over the life of the loan.

Here is how the landscape generally breaks down:

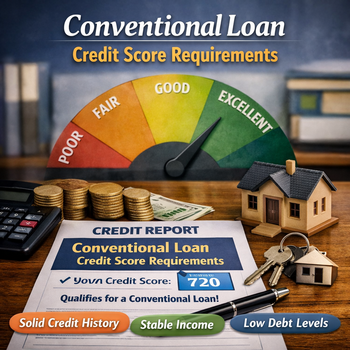

1. Excellent (760 – 850)

Suppose your score is above 760, congratulations. You are in the top tier. Lenders view you as a minimal risk. You will qualify for the absolute lowest available interest rates and the smallest down payment options (as low as 3%) without incurring significant pricing penalties.

2. Good (700 – 759)

This is the sweet spot for the average American homebuyer. You will still qualify for very competitive rates. While you might pay a slightly higher rate than the 760+ club, the difference is usually marginal. Most lenders are very comfortable approving borrowers in this range.

3. Fair (620 – 699)

This is where things get expensive. If you fall into this range, you can still get a conventional loan, but you will face several hurdles:

- Higher Interest Rates: You will be subject to steeper LLPAs, meaning your monthly payment will be significantly higher than someone with a 720 score.

- Higher Down Payment Requirements: While conventional loans can go as low as 3% down, borrowers with scores in the low 600s may be required to put down 5%, 10%, or even 25% to offset the risk.

- Stricter Debt-to-Income (DTI) Ratios: Lenders may limit your total monthly debts (including the new mortgage) to 36% or 43% of your gross income, whereas a high-credit-score borrower might be allowed to go up to 50%.

4. Poor (Below 620)

If your score is below 620, a conventional loan is generally off the table. You will not meet Fannie Mae or Freddie Mac’s minimum requirements. However, this does not mean homeownership is impossible. Borrowers in this range typically turn to FHA loans, which allow for scores as low as 580 (or even 500 with 10% down).

Beyond the Number: What Lenders Actually Look At

While the three-digit number is critical, conventional loan underwriting is holistic. Lenders will also scrutinize:

- Credit History: Do you have a recent bankruptcy (usually a 4-year wait for conventional loans) or foreclosure (usually a 7-year wait)? A high score won’t matter if you have a major derogatory event that hasn’t aged enough.

- Reserves: For borrowers with lower scores (620-680), lenders often require "reserves"—cash in the bank equivalent to 2 to 6 months of mortgage payments. This acts as a safety net to prove you can handle the payment if your income is interrupted.

- Down Payment Source: With a high credit score, a "gift" from a family member for the down payment is usually fine. With a lower score, lenders often want to see that the money came from your savings and has been "seasoned" (sitting in your account) for at least 60 days.

Conventional vs. FHA: The Great Debate

If your score is between 580 and 620, you face a common dilemma: Should I fix my credit to get a conventional loan, or take an FHA loan now?

| Feature | Conventional Loan | FHA Loan |

|---|---|---|

| Min Credit Score | 620 | 580 (or lower with 10% down) |

| Mortgage Insurance | Cancels once you reach 20% equity. | Usually lasts for the life of the loan (or 11 years if 10% down). |

| Upfront Cost | Low upfront fees. | Requires 1.75% upfront mortgage insurance premium (MIP). |

| Interest Rates | Risk-based (higher score = lower rate). | Generally, the same rate for everyone, regardless of score. |

The Verdict: If your score is 620, a conventional loan is usually the better long-term financial move because you can eventually drop private mortgage insurance (PMI). If your score is 580, FHA is likely your only path, but you should plan to refinance into a conventional loan later if your credit improves.

How to Boost Your Score Before You Apply

If you are hovering near the 620 threshold, it pays to wait. Raising your score by just 20 to 40 points can save you thousands of dollars in interest and eliminate strict reserve requirements.

- Pay Down Credit Card Balances: This is the fastest way to raise your score. Credit utilization (the ratio of your balance to your credit limit) makes up 30% of your score. Try to get each card below 30% utilization, and ideally below 10%.

- Do Not Close Old Accounts: Length of credit history matters. If you have old no-annual-fee credit cards, keep them open, even if you don’t use them.

- Stop Applying for New Credit: In the 6 to 12 months leading up to a mortgage application, avoid opening new credit cards or car loans. Each hard inquiry dings your score temporarily.

- Dispute Errors: Obtain a free copy of your credit report from AnnualCreditReport.com. Dispute any collection accounts that aren’t yours, or try to negotiate a "pay-for-delete" with collection agencies for small, old debts.

The Bottom Line

A conventional loan offers the most favorable terms for homeowners who can meet the credit requirements. While the technical minimum is 620, the reality is that the best deals—lowest rates, lowest down payments, and easiest approvals—are reserved for borrowers with scores above 680, and preferably above 740.

Before you fall in love with a house, fall in love with your credit score. Taking six months to improve your financial profile isn’t a delay; it’s an investment that will likely save you tens of thousands of dollars over the 30-year life of your loan.

Disclaimer: This article is for informational purposes only and does not constitute financial or legal advice. Mortgage guidelines, interest rates, and credit score requirements change frequently. Please consult with a licensed mortgage loan officer for current information specific to your financial situation.

Connect With Us

Please share – it really helps