What Are USDA Loans in Pennsylvania and How Do They Work?

Are you thinking about buying a home in Pennsylvania

but worried about a big down payment or high interest rates? USDA

loans might be the solution you’ve been searching for.

Are you thinking about buying a home in Pennsylvania

but worried about a big down payment or high interest rates? USDA

loans might be the solution you’ve been searching for.

These special loans are designed to help people like you buy homes in rural and suburban areas with low or no down payment. But how exactly do USDA loans in PA work, and could they be the right fit for your situation?

Keep reading to discover how these loans can make homeownership easier and more affordable for you.

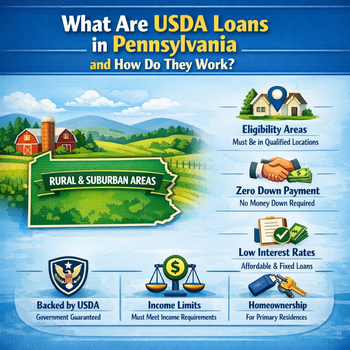

Basics of USDA Loans

USDA loans help many people buy homes in rural and suburban areas. These loans come from the U.S. Department of Agriculture. They aim to support families with low to moderate income. USDA loans often offer benefits that other loans do not. Understanding these basics can help decide if a USDA loan fits your needs.

USDA loans focus on making home buying easier and more affordable. They usually require no down payment. This feature lowers the upfront cost of buying a home. The loans also have competitive interest rates. These rates often stay lower than conventional loan rates. This can save money over time.

What Is A Usda Loan?

A USDA loan is a mortgage backed by the U.S. government. It helps buyers purchase homes in eligible rural areas. The goal is to boost rural development. The loan supports families who may struggle to get traditional loans. It offers a path to homeownership with less financial pressure.

Who Qualifies For Usda Loans?

Qualification depends on income and location. The home must be in an area approved by the USDA. The buyer's income should be within USDA limits. These limits vary by county and family size. The loan targets low to moderate-income families. Credit score and debt also affect eligibility.

Key Features of USDA Loans

No down payment is one major feature. This makes buying a home easier. The loan also includes low mortgage insurance costs. This keeps monthly payments affordable. USDA loans offer fixed interest rates. The loan term usually lasts 30 years. The process may require a home appraisal and property inspection.

Eligibility Criteria In Pennsylvania

USDA loans offer a unique chance for many Pennsylvanians to buy homes at low costs. These loans focus on helping buyers in rural areas. The eligibility rules ensure the right people get this support. Understanding these rules helps you see if this loan fits your needs.

Location Requirements

USDA loans are for homes in rural parts of Pennsylvania. The USDA uses maps to define these areas. Towns with small populations often qualify. Some suburbs may also meet the rules. Check the USDA site to find eligible locations.

Income Limits

Your household income must be within certain limits. These limits depend on your county and family size. The goal is to help low to moderate-income families. Income includes all adults living in the home. Some income types might not count.

Credit Score And Financial History

The USDA needs a good credit history. Usually, a score of 640 or higher is needed. This shows you can pay back the loan. Past bankruptcies or foreclosures may affect approval. Lenders look at your debts and payment history.

Property Standards

The home must be your main residence. It must meet safety and quality standards. The property should not be used for business. The house must be in good condition. The USDA may require repairs before approval.

Citizenship And Residency

Applicants must be U.S. citizens or permanent residents. Non-citizens usually cannot apply. You must live in the home after buying it. The loan is not for investment or rental properties.

Types of USDA Loans Available

USDA loans offer different types tailored to various needs. Understanding each type helps choose the right loan. These loans assist low to moderate-income buyers in rural areas. They provide affordable home financing options.

Direct Loans

Direct loans come straight from the USDA. They help buyers with low incomes. These loans have low-interest rates. They often require little or no down payment. The USDA manages the entire loan process.

Guaranteed Loans

Guaranteed loans involve private lenders. The USDA guarantees part of the loan. This reduces risk for lenders. These loans help moderate-income buyers. They require no down payment, too.

Home Repair Loans And Grants

This option supports home repairs for low-income owners. Loans cover major repairs and improvements. Grants help elderly homeowners with urgent repairs. Both improve home safety and comfort.

Application Process Steps

The application process for USDA loans in Pennsylvania follows clear steps. Each step helps you move closer to homeownership. Understanding the process lowers stress and speeds up approval.

Below are the main steps you will take when applying for a USDA loan.

Check Eligibility

First, check if your property is in a USDA-eligible area. USDA loans focus on rural and suburban locations. Also, review income limits to ensure you qualify. Your household income must be within the allowed range.

Gather Required Documents

Prepare documents like proof of income, tax returns, and credit reports. You will also need identification and information about debts. Having these ready makes the process smoother.

Find a USDA-approved Lender

Choose a lender approved to offer USDA loans. These lenders understand USDA rules and guide you properly. The lender will help you start the application and explain the terms.

Complete The Loan Application

Fill out the loan application form with accurate details. Provide information about your finances, employment, and the property. The lender will review the application carefully.

Property Appraisal And Inspection

The USDA requires a property appraisal to check the value and condition. The home must meet USDA property standards. The lender arranges this step after initial approval.

Loan Processing And Underwriting

During processing, the lender verifies all information. The underwriter reviews your file to ensure it meets USDA rules. They decide if the loan can be approved.

Loan Approval And Closing

Once approved, you receive a loan commitment letter. You will then schedule a closing date. At closing, sign documents and pay any closing costs. After closing, you get the keys to your home.

Benefitsof USDAa Loans

USDA loans offer many benefits for homebuyers in Pennsylvania. They help people buy homes with less money up front. These loans support rural and suburban areas, making homeownership easier. Understanding the benefits can help you decide if a USDA loan is right for you. The government backs these loans, so lenders often offer better terms. They make buying a home affordable for many families. Let’s explore the key benefits of USDA loans in PA.

Low Or No Down Payment

USDA loans often require zero down payment. This means buyers don’t need to save a large amount before making a purchase. It helps families with limited savings buy a home sooner. A low or no down payment reduces the initial cost of buying a house.

Competitive Interest Rates

Interest rates on USDA loans tend to be lower than those on other loans. This makes monthly payments smaller. Lower rates save money over the life of the loan. It helps buyers afford homes with less financial stress.

Flexible Credit Guidelines

USDA loans allow for flexible credit scores. Borrowers with less-than-perfect credit may still qualify. This opens the door for many who struggle with credit history. It increases the likelihood of owning a home despite past credit issues.

Reduced Mortgage Insurance Costs

USDA loans have lower mortgage insurance fees than other loans. This reduces monthly payments further. It makes the loan more affordable over time. Lower insurance costs help keep homeownership within reach.

Supports Rural And Suburban Communities

USDA loans focus on helping buyers in rural and some suburban areas. This supports growth in less populated communities. It encourages homeownership where it’s needed most. The program helps build strong, vibrant neighborhoods.

Common Challenges And Solutions

USDA loans in Pennsylvania offer many benefits but come with some challenges. Knowing common problems helps buyers prepare better. Solutions make the process smoother and increase the chances of approval.

Understanding Income Limits

USDA loans require income below a set limit. Many buyers find this limit confusing. It varies by county and family size. Checking local USDA guidelines helps avoid surprises. Using online calculators can quickly clarify eligibility.

Meeting Property Eligibility

Only homes in rural areas qualify for USDA loans. Some buyers struggle to find eligible properties. The USDA website lists approved locations. Contacting local agents familiar with USDA rules saves time. Exploring nearby towns may reveal more options.

Handling Credit Score Requirements

USDA loans need a credit score of about 640. Low scores can block approval. Improving credit by paying bills on time helps. Some lenders accept alternative credit data. Asking lenders about options can open doors.

Dealing With Debt-to-Income Ratio

High debt makes USDA loan approval harder. The maximum ratio is about 41%. Reducing debts before applying improves chances. Consolidating loans or paying off small debts helps. Lenders may also consider compensating factors.

Managing Appraisal And Inspection Issues

USDA loans require a home appraisal. Problems like needed repairs can delay loans. Fixing major issues before the appraisal prevents delays. Sellers often agree to repairs or price reductions. A clear inspection report supports loan approval.

Comparing USDA Loans With Other Options

Comparing USDA loans with other home loan options helps buyers in Pennsylvania choose the best fit. Each loan type has unique features and benefits. Understanding these differences can save money and time.

Comparing USDA Loans And Conventional Loans

USDA loans offer zero down payment. Conventional loans often require 5% to 20% down. USDA loans focus on rural areas. Conventional loans work anywhere. USDA loans have income limits. Conventional loans do not. USDA loans include mortgage insurance. Conventional loans may need private mortgage insurance.

Comparing USDA Loans and FHA Loans

FHA loans require a small down payment, usually 3.5%. USDA loans need no down payment. FHA loans have more flexible credit score rules. USDA loans require good credit history. FHA loans work in all locations. USDA loans target rural and suburban areas. Both have mortgage insurance costs, but USDA's may be lower.

Comparing USDA Loans And Va Loans

VA loans are for veterans and active military members. USDA loans are for rural homebuyers with low- to moderate-income. VA loans usually have no down payment or mortgage insurance. USDA loans require mortgage insurance. Both offer competitive interest rates. Eligibility rules differ greatly between these loan types.

Frequently Asked Questions

What Are USDA Loans In Pa?

USDA loans in PA are government-backed home loans for rural areas. They help buyers with low to moderate income buy homes with no down payment.

Who Qualifies For A USDA Loan In Pennsylvania?

You must live in an eligible rural area and meet income limits. Credit history should show the ability to pay, but requirements are flexible.

How Do USDA Loans Work In Pennsylvania?

The USDA guarantees a portion of the loan, lowering risk for lenders. This allows buyers to get loans with no down payment and low interest rates.

What Types Of Homes Can USDA Loans Buy In Pa?

USDA loans cover single-family homes in approved rural areas. The home must be your primary residence and meet basic safety standards.

What Are The Benefits of USDA Loans In Pennsylvania?

USDA loans offer zero down payment and low mortgage insurance. They also have competitive interest rates compared to conventional loans.

Conclusion

USDA loans in PA help many people buy homes at low costs. They offer no down payment and low interest rates. This makes buying a home easier for families in rural areas. Knowing how these loans work can guide you to smart choices.

Explore your options carefully and see if you qualify. A USDA loan might be the right step toward your new home. Keep learning and ask questions to make the best decision.

Connect With Us

Please share – it really helps