Conventional Loan Debt-to-Income Ratio Requirements

When

applying for a conventional mortgage, few numbers carry as much

weight as your Debt-to-Income (DTI) ratio. It is one of the

primary metrics lenders use to assess risk, determining not just

if you qualify for a loan, but often the terms

and interest rate you will receive.

When

applying for a conventional mortgage, few numbers carry as much

weight as your Debt-to-Income (DTI) ratio. It is one of the

primary metrics lenders use to assess risk, determining not just

if you qualify for a loan, but often the terms

and interest rate you will receive.

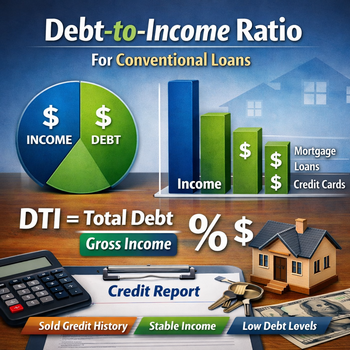

While credit scores reflect your history of paying back Debt, the DTI ratio reflects your capacity to take on new Debt. For conventional loans—mortgages backed by Fannie Mae and Freddie Mac—this ratio is a gatekeeper to approval.

What is DTI?

The Debt-to-Income ratio is a simple percentage that represents how much of your gross monthly income goes toward paying debts.

There are two distinct types of DTI that lenders analyze:

1. Front-End Ratio (Housing Ratio)

This calculates the percentage of your gross monthly income that goes solely toward housing expenses. For a conventional loan, this includes:

- Principal & Interest (the loan payment)

- Property Taxes

- Homeowners Insurance

- Mortgage Insurance (if your down payment is less than 20%)

The Formula: (Total Monthly Housing Payment) ÷ (Gross Monthly Income) = Front-End DTI

2. Back-End Ratio (Total DTI)

This is the more critical of the two numbers. It calculates the percentage of your gross monthly income that goes toward all recurring debt obligations, including the new housing payment.

- Credit card minimum payments

- Auto loans and leases

- Student loans

- Personal loans

- Alimony or child support

- The new proposed housing payment

The Formula: (Total Monthly Debt + New Housing Payment) ÷ (Gross Monthly Income) = Back-End DTI

The Conventional Loan Limits

Conventional loans follow underwriting standards set by Fannie Mae and Freddie Mac. While these entities allow for some flexibility depending on the strength of the borrower (high credit score, large reserves), the standard "gold standard" thresholds are as follows:

- Ideal Ratio: 36% Back-End DTI. This is the traditional benchmark. Borrowers with a DTI of 36% or lower are generally considered low-risk and typically qualify for the best interest rates and terms.

- Manual Underwriting Limit: 43% Back-End DTI. For a long time, 43% was the hard cap for a "Qualified Mortgage" (QM). While automated underwriting systems (AUS) like Fannie Mae’s Desktop Underwriter (DU) can approve ratios above this threshold, a DTI exceeding 43% requires significant compensating factors.

- Maximum via Automated Approval:

Up to 50% (Under Specific Conditions). It is

possible to get a conventional loan with a back-end DTI of

45% to 50%. However, this is only possible if the borrower

has:

- A very high credit score (typically 720 or above)

- Significant liquid reserves (6 to 12 months of mortgage payments in the bank)

- A large down payment (20% or more)

Note: If your down payment is less than 20%, the back-end DTI ratio is usually stricter, often capped at 43% to 45%, because the presence of Private Mortgage Insurance (PMI) adds to monthly payments and increases the lender's risk.

How to Calculate Your DTI

To determine where you stand, follow these steps:

Step 1: Calculate Gross Monthly Income. Add up all sources of stable income before taxes. This includes salary, hourly wages, commissions (averaged over 2 years), bonuses, and any consistent rental income.

Step 2: Calculate Total Monthly Recurring Debts. Pull your credit report. Add up the minimum monthly payments for all liabilities listed above. Do not include utilities, car insurance, cell phone bills, or health insurance, as these are not considered "debt" for DTI purposes.

Step 3: Add the Proposed Housing Payment. Use an online mortgage calculator to estimate the full PITIA (Principal, Interest, Taxes, Insurance, and HOA dues if applicable).

Step 4: Do the Math (Debts + Housing) ÷ Gross Income = DTI

Example:

- Gross Monthly Income: $8,000

- Car Payment: $400

- Credit Cards: $200

- Student Loans: $300

- Proposed Mortgage Payment: $2,100

Total Debt: $3,000 DTI: $3,000 ÷ $8,000 = 37.5%

In this scenario, the borrower falls within the acceptable range for a conventional loan.

Strategies to Improve Your DTI

If your DTI exceeds the lender’s threshold, you are not necessarily out of options. Here are the three most effective strategies to improve your ratio:

1. Pay Down Revolving Debt

Credit cards are the easiest Debt to fix. Because lenders use the minimum payment on your credit report, paying down a balance significantly reduces that minimum payment. Even if you pay off a card entirely, the minimum payment drops to $0, instantly improving your DTI.

2. Extend Loan Terms (Auto or Student Loans)

If you are close to the limit, you can sometimes refinance an auto or student loan into a longer term. This lowers the monthly payment, thereby lowering the DTI. Note: This strategy increases the total Interest paid over time, so it should be used strategically for qualification purposes.

3. Increase Your Down Payment

A larger down payment reduces the loan amount, which reduces the principal and interest portion of the monthly housing payment. If you are currently carrying mortgage insurance, putting down 20% eliminates that expense, which can lower your DTI by several percentage points.

4. Use a Co-Borrower

If the property is a primary residence, adding a co-borrower (such as a spouse or family member) with stable income can combine incomes to lower the overall ratio, provided their debts are also factored in.

DTI vs. The Rest of Your Application

It is crucial to understand that DTI does not exist in a vacuum. Conventional loans rely heavily on Automated Underwriting (AUS). The system evaluates the entire risk profile together.

A borrower with a 780 credit score and 12 months of cash reserves might be approved for a conventional loan with a 49% DTI. Conversely, a borrower with a 640 credit score and a 43% DTI might be denied.

Lenders look at the "Three C's of Credit":

- Capacity: Your DTI

- Credit: Your score and history

- Collateral: The down payment and property value

If your DTI is high, you must have exceptionally strong Credit and Collateral to offset the risk.

Disclaimer: This content is for informational purposes only and does not constitute financial or legal advice. Conventional loan guidelines are subject to change. Please consult with a licensed mortgage loan originator for specific qualification requirements.

Connect With Us

Please share – it really helps