Conventional Loan Down Payment Requirements for 2026

For decades, the 20% down payment was the gold standard for

homebuyers—a daunting sum that kept many aspiring homeowners on the

sidelines. But today, the landscape has shifted dramatically. In

2026, conventional loans offer unprecedented flexibility, with

qualified buyers securing homes for as little as 3% down .

For decades, the 20% down payment was the gold standard for

homebuyers—a daunting sum that kept many aspiring homeowners on the

sidelines. But today, the landscape has shifted dramatically. In

2026, conventional loans offer unprecedented flexibility, with

qualified buyers securing homes for as little as 3% down .

Understanding these requirements is essential whether you're buying your first home or adding to your investment portfolio. Let's explore exactly how much you'll need, how to qualify, and the trade-offs that come with different down payment amounts.

What Is a Conventional Loan?

A conventional loan is a mortgage not insured or guaranteed by the federal government. Unlike FHA, VA, or USDA loans, conventional financing follows guidelines set by Fannie Mae and Freddie Mac—government-sponsored enterprises that purchase most U.S. mortgages .

These loans dominate the housing market, accounting for approximately 73% of single-family home purchases. Their popularity stems from competitive interest rates, flexible terms, and broad availability .

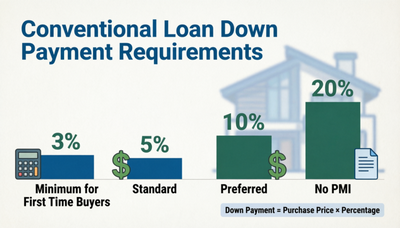

Minimum Down Payment Requirements by Buyer Type

The minimum down payment for a conventional loan depends primarily on your buyer status and property type. Here's how the requirements break down in 2026:

| Scenario | Minimum Down Payment |

|---|---|

| First-time homebuyers (primary residence) | 3% |

| Repeat buyers (primary residence) | 5% |

| Second homes | 10%–15% |

| Multi-unit investment properties | 15%–25% |

Source:

Who Qualifies as a First-Time Homebuyer?

The definition is broader than you might expect. Lenders typically consider anyone who has not owned a home in the past three years as a first-time homebuyer . This means if you sold your previous home three or more years ago, you may regain eligibility for 3% down programs.

Special 3% Down Programs

Several specific programs enable qualified buyers to access 3% down financing:

-

Conventional 97: Allows financing up to 97% of the purchase price. Requires at least one borrower to be a first-time homebuyer, and first-timers must complete an approved homebuyer education course. No income limits apply .

-

Fannie Mae HomeReady: Designed for low- to moderate-income borrowers. Household income generally must fall below 80% of the area median income. First-time buyer status is not required, and the program allows non-borrower household income to help with qualification .

-

Freddie Mac Home Possible: Similar to HomeReady, this program offers 3% down financing for low- to moderate-income buyers. First-time buyers must complete a homeownership education course. One distinct advantage: co-borrowers who don't live in the residence can contribute financially .

The 20% Myth: Understanding Private Mortgage Insurance

You've likely heard that you need 20% down to buy a home. This is a common misconception. In reality, 20% down is only required if you want to avoid Private Mortgage Insurance (PMI) .

What Is PMI?

PMI protects the lender if you default on your loan. It's required on all conventional loans with down payments below 20% until you build sufficient equity . The cost typically ranges from 0.3% to 1.5% of your loan amount annually, broken into monthly payments .

How PMI Costs Compare by Down Payment

| Down Payment | PMI Required? | Approximate Monthly PMI (on $400,000 home) |

|---|---|---|

| 3% | Yes | $97–$485 |

| 5% | Yes | $95–$475 |

| 10% | Yes | $90–$450 |

| 20%+ | No | $0 |

Source:

How to Eliminate PMI

PMI isn't permanent. You can request cancellation once your loan-to-value ratio reaches 80% (meaning you have 20% equity). Under the Homeowners Protection Act, PMI must automatically terminate when your loan-to-value reaches 78% .

Additional Qualification Requirements

Your down payment is just one piece of the puzzle. To qualify for a conventional loan, you'll also need to meet these standards:

Credit Score

- Minimum: Typically 620, though Fannie Mae and Freddie Mac eliminated strict minimums in late 2025

- Optimal: Scores above 740 secure the best interest rates

- Impact: Higher scores can offset other weaknesses, potentially allowing up to 50% debt-to-income ratios

Debt-to-Income Ratio (DTI)

Lenders prefer your total monthly debts—including the new mortgage payment—to stay at or below 43% of your gross monthly income. Strong credit profiles may allow up to 50% .

Income and Employment Stability

Expect to provide:

- Recent pay stubs (typically 30 days)

- W-2 forms from the past two years

- Tax returns (especially if self-employed)

- Proof of continued employment throughout the process

Cash Reserves

While not always required for primary residences, having 2 to 6 months of mortgage payments in reserve strengthens your application. Second homes and investment properties typically require more .

Conforming Loan Limits for 2026

The amount you can borrow while keeping conventional loan status depends on your location. The Federal Housing Finance Agency (FHFA) sets conforming loan limits annually based on home price appreciation .

2026 Baseline Limits

| Property Type | Standard Areas | High-Cost Areas |

|---|---|---|

| 1 unit | $832,750 | $1,249,125 |

| 2 units | $1,066,250 | $1,599,375 |

| 3 units | $1,288,800 | $1,933,200 |

| 4 units | $1,601,750 | $2,402,625 |

Source:

What If You Need to Borrow More?

Loans exceeding these limits are called jumbo loans. While still conventional (non-government), they come with stricter requirements:

- Credit scores typically 700 or higher

- Minimum down payments of 10% to 25%

- 6 to 12 months of cash reserves

- Lower maximum DTI ratios (usually 43%)

The Real-World Impact of Your Down Payment Choice

Your down payment affects more than just your upfront cash requirement. Consider these scenarios for a $400,000 home purchase:

| Down Payment | Loan Amount | Monthly Payment (est.) | PMI | Total Interest Over 30 Years |

|---|---|---|---|---|

| 3% ($12,000) | $388,000 | Higher | Yes | Highest |

| 5% ($20,000) | $380,000 | Moderate | Yes | Moderate-high |

| 10% ($40,000) | $360,000 | Lower | Yes | Moderate |

| 20% ($80,000) | $320,000 | Lowest | No | Lowest |

Note: Monthly payments and interest calculations vary by rate and terms.

Advantages of a Smaller Down Payment

- Earlier homeownership: Enter the market sooner rather than waiting years to save

- Preserved savings: Keep cash available for emergencies, repairs, or furnishings

- Investment flexibility: Use remaining funds for other financial goals

Advantages of a Larger Down Payment

- No PMI: Save hundreds monthly once you reach 20%

- Lower monthly payments: Less debt service improves cash flow

- Better interest rates: Lenders often offer better pricing

- More equity: Greater protection against market downturns

Sources of Down Payment Funds

Lenders are particular about where your down payment comes from. Acceptable sources include:

- Personal savings: The most straightforward source, requiring bank statements showing funds "seasoned" for at least 60 days

- Gift funds: Family members, employers, churches, or nonprofit organizations can contribute. Requires a gift letter confirming no repayment obligation

- Down payment assistance programs: Many state and local programs offer grants or low-interest loans to qualified buyers

Restrictions to Know

Gift funds for second homes and investment properties face tighter restrictions. Additionally, some 3% down programs may require the borrower to contribute at least some personal funds .

Steps to Strengthen Your Application

If you're concerned about qualifying, consider these strategies:

-

Boost your credit score: Pay down credit card balances to below 30% of limits, address any delinquencies, and avoid new credit applications for six months before applying .

-

Lower your DTI: Pay off small debts to reduce your monthly obligations. Even paying off a car loan or credit card can make a significant difference .

-

Save more than the minimum: While 3% may qualify you, putting 5% to 10% down improves your chances and reduces PMI costs .

-

Shop multiple lenders: Requirements vary. Some lenders offer more flexibility on credit scores or DTI ratios than others .

The Bottom Line

Conventional loans in 2026 offer remarkable accessibility, with down payments starting at just 3% for qualified first-time buyers. While the traditional 20% down payment remains the surest path to avoiding PMI and securing the lowest monthly payment, it's no longer a barrier to entry.

The right down payment for you depends on your financial situation, local housing market, and long-term goals. If you have stable income, good credit, and want to enter the market now, a 3% or 5% down conventional loan can be a smart move. If you're close to saving 20% and can wait, the long-term savings on PMI and interest may be worth it.

Whatever path you choose, start by getting pre-approved with multiple lenders. With personalized Loan Estimates in hand, you can compare real numbers and make the decision that best fits your financial future .

This article provides general information and does not constitute financial advice. Consult with a qualified mortgage professional regarding your specific situation.

Connect With Us

Please share – it really helps