Conventional Loan Gift Funds: Rules and How to Use Them

In the intricate ballet of buying a home, few moments are as pivotal—or as fraught with peril—as the sourcing of the down payment. For a vast swath of aspiring homeowners, the dream is not funded by a liquidation event or a decade of scrimping in a high-yield savings account. It is funded by love. It comes from parents, grandparents, or sometimes a generous sibling.

In the intricate ballet of buying a home, few moments are as pivotal—or as fraught with peril—as the sourcing of the down payment. For a vast swath of aspiring homeowners, the dream is not funded by a liquidation event or a decade of scrimping in a high-yield savings account. It is funded by love. It comes from parents, grandparents, or sometimes a generous sibling.

This is gift funds.

But in the eyes of a conventional lender, a gift is not simply a warm transaction. It is a potential liability, a variable to be stress-tested, and a trail of paper to be audited. While gift funds are a perfectly legitimate and common way to purchase a home, the rules governing them for conventional loans (backed by Fannie Mae and Freddie Mac) are specific, unforgiving, and often misunderstood.

If you are planning to accept a financial gift to buy a home, you are not just receiving generosity; you are entering a compliance exercise. Here is how to navigate it without derailing your mortgage.

The Fundamental Divide: Conventional vs. Government Loans

Before diving into the mechanics, it is crucial to understand why conventional loans treat gifts differently than their government-backed cousins (FHA, VA, USDA).

FHA and VA loans are generally more permissive. They allow gifts for the entire down payment and closing costs with relatively straightforward documentation. Conventional loans (those backed by Fannie Mae and Freddie Mac) operate on a risk-based model tied to loan-to-value (LTV) ratios. This leads to the most important distinction in conventional lending: the LTV threshold.

The Critical Rule: Property Type Determines Gift Fund Requirements

The key to understanding gift fund rules for conventional loans is understanding that Fannie Mae treats single-family homes (1-unit primary residences) very differently from multi-unit properties and second homes. The rules are based on both property type and loan-to-value (LTV)—the ratio of your loan amount to the property's appraised value or purchase price, whichever is lower.

Here is the table that governs all gift fund transactions:

| Property Type | LTV ≤ 80% | LTV > 80% |

|---|---|---|

| 1-Unit Primary Residence | Gift funds can cover 100% of down payment and closing costs. No borrower contribution required. | Gift funds can cover 100% of down payment and closing costs. No borrower contribution required. |

| 2-4 Unit Primary Residence | Gift funds can cover 100% of down payment and closing costs. No borrower contribution required. | Borrower must contribute minimum 5% from personal funds. Gift funds can cover the remaining down payment and closing costs. |

| Second Home (1-4 units) | Gift funds can cover 100% of down payment and closing costs. No borrower contribution required. | Borrower must contribute minimum 5% from personal funds. Gift funds can cover the remaining down payment and closing costs. |

| Investment Property | Gifts are NOT allowed. Borrower's own funds must cover the entire down payment. | |

Example 1 (1-Unit Primary Residence, LTV 85%): You are buying a single-family home for $400,000 with 15% down ($60,000). Your LTV is 85%. Even though your LTV exceeds 80%, you are allowed to use gift funds to cover the entire $60,000 down payment. No personal contribution from you is required because this is a 1-unit primary residence.

Example 2 (2-Unit Primary Residence, LTV 85%): You are buying a duplex for $400,000 with 15% down ($60,000). Your LTV is 85%. Because your LTV exceeds 80% and this is a 2-unit property, you must contribute at least 5% of the purchase price ($20,000) from your own verified funds. The remaining $40,000 can be a gift.

Example 3 (1-Unit Primary Residence, LTV 50%): You are buying a single-family home for $400,000 with 50% down ($200,000). Your LTV is 50%. The entire $200,000 can be a gift. This is the most flexible scenario because both property type and LTV are in your favor.

This distinction is critical. If you are buying a single-family primary residence, you have maximum flexibility with gift funds regardless of your LTV. If you are buying a multi-unit property or a second home with an LTV above 80%, you must reserve 5% of the purchase price from your own pocket.

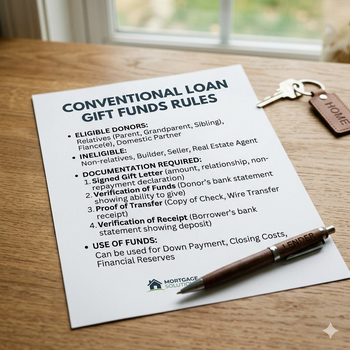

Who Can Give the Gift?

Lenders are not just looking for money; they are looking for provenance. The source of the gift matters immensely. For conventional loans, the donor must be an acceptable source. Fannie Mae's guidelines define acceptable donors as:

- Spouse, child, or dependent

- Parent, grandparent, or great-grandparent

- Sibling, grandchild, or great-grandchild

- Domestic partner

- Fiancé or fiancée (though the marriage must occur before closing)

- Non-relatives who share a familial relationship, such as a former relative, godparent, or individual with a long-standing familial-like or mentorship relationship

Non-Allowable Donors: You generally cannot use gift funds from uncles, aunts, cousins, friends, or the seller who has a financial interest in the transaction. However, a seller can provide a gift of equity if they are not affiliated with any other interested party.

The Paper Trail: The Gift Letter and Sourcing

If there is a mantra in mortgage underwriting, it is this: If it isn't documented, it doesn't exist.

Gift funds trigger a forensic audit of your bank statements. Here is how to survive it.

1. The Gift Letter

Every donor must sign a formal "Gift Letter." This is not a casual note; it is a legally binding document that states:

- The donor's name, address, and relationship to the borrower

- The exact dollar amount of the gift

- The address of the property being purchased

- A clear statement that the funds are a gift and require no repayment

This last point is critical. If there is any whiff that the money is a loan—even a handshake agreement to pay it back later—the underwriter will treat it as debt. That debt will be calculated into your debt-to-income (DTI) ratio, potentially disqualifying you for the loan.

2. Sourcing and Seasoning

Lenders need to verify that the donor actually has the money and that it is not sourced from prohibited channels (e.g., an unsecured loan from the donor's credit card).

If the gift is transferred before you apply: The money will appear in your bank account. The lender will ask for your last two months of bank statements. If a large, unusual deposit appears (the gift), you will need to provide the donor's bank statement showing the funds leaving their account, plus the gift letter.

If the gift is transferred at closing: This is the cleaner method. The donor can wire the funds directly to the title company or escrow officer at closing. In this case, the lender only needs the donor's bank statement showing the funds were available, the gift letter, and proof of the wire.

3. The "Seasoned" Deposit Rule

If a donor transfers the money to you months before you apply for a loan, it becomes "seasoned." If the deposit appears on a bank statement older than the two-month lookback period, you do not need to source it. However, timing is everything. If you receive the gift, deposit it, and then apply for a loan two weeks later, that deposit will be flagged.

Common Pitfalls and How to Avoid Them

Even with the best intentions, gift funds are a leading cause of closing delays. Here are the most common traps.

The Cash Handoff

Lenders do not accept cash. If a relative hands you $10,000 in physical currency, that money is effectively toxic to a mortgage application. You cannot deposit it and claim it as a gift without a provable paper trail from the donor's withdrawal. If the donor withdraws cash, they have broken the chain of custody. To fix this, the donor must deposit the cash back into their account and issue a cashier's check or wire.

The Floating Bank Account

Donors often move money between accounts (savings to checking) right before sending it. If the donor's bank statement shows a transfer in from an unknown account, the underwriter will ask to see the source account as well. To avoid this, ask your donor to keep the gift funds in a single, liquid account for at least two months before the wire.

The Employer/Partner Loophole

Some borrowers attempt to have their employer or business partner give them a "bonus" or gift to help with the down payment. Conventional guidelines generally prohibit this unless the employer is a documented down payment assistance program. If the money comes from a business entity (LLC, corporation), the underwriter will assume it is a loan against the business, which is rarely allowed.

Strategic Considerations for Borrowers

If you are using gift funds, you are playing a high-stakes game of logistics. To ensure a smooth closing, consider the following strategies:

Disclose early. Tell your loan officer about the gift on day one. Do not wait for underwriting to ask. A good loan officer will structure the file to ensure compliance from the outset.

Know your property type and LTV. The critical distinction is whether you are buying a 1-unit primary residence or a different property type. If you are buying a 1-unit primary residence, you have complete flexibility with gift funds regardless of your down payment percentage. If you are buying a 2-4 unit property or a second home with an LTV above 80%, ensure you have your own 5% contribution ready.

Separate accounts. If you must make a borrower contribution, keep your own funds in a separate account from the gift funds. This simplifies the sourcing process for the underwriter, who must trace which funds are yours and which are gifted.

Consider a non-occupant co-borrower. If a parent wants to help but the logistics of a gift are too complex (particularly for 2-4 unit properties or second homes above 80% LTV), they can be added to the loan as a non-occupant co-borrower. This allows them to use their income and assets to qualify, though it also puts them on the hook for the debt.

Conclusion

Gift funds are a powerful tool for building wealth and achieving homeownership. They represent intergenerational support and familial stability. However, the conventional loan framework treats them with a healthy skepticism, viewing them as a potential source of fraud or unverified debt.

To succeed, you must treat the gift not as a simple transfer of love, but as a key piece of evidence in a financial audit. Understand your property type and LTV using the table provided in this article. For 1-unit primary residences, you have maximum flexibility with gifts at any LTV. For 2-4 unit properties and second homes above 80% LTV, you must have 5% from your own pocket. Keep the paper trail pristine. Ensure the gift letter is signed, dated, and unequivocal.

When managed correctly, gift funds allow borrowers to achieve better loan terms, avoid private mortgage insurance (PMI) sooner, and step onto the property ladder with the support of those who believe in them most. When managed poorly, they cause heartbreak and delayed closings.

Understand the rules, communicate with your lender, and give your donor clear instructions. In the world of real estate, a gift is only as good as the paper it's printed on.

Connect With Us

Please share – it really helps